2025 Business Predictions: Andrew Bridge, Managing Partner of Fisher German

It’s that time of year, when Business Link Magazine invites the region’s business leaders to offer up their predictions for the year ahead.

It has become something of a tradition, given that we’ve been doing this now for over 30 years.

Here we speak to Andrew Bridge, Managing Partner at property consultancy Fisher German.

Despite a challenging picture for businesses following the Budget in October, there will still be potential for growth in 2025.

The recent NPPF reforms were welcome, but it remains to be seen how effective it will be in delivering the housing the country needs. Inflation and interest rates may continue to slow down the residential market, with the cost of borrowing being a major factor in successful transactions.

Commercial growth may also be hindered by a lack of land supply and reliable grid connections, making it difficult for companies to expand.

However, the rise in national insurance contributions, while challenging for many businesses, could actually result in opportunities for further work.

The National Wealth Fund, a government initiative set up to attract private investment in clean energy and growth industries, is set to invest a further £5.8bn of capital into these projects during this Parliament, which the increase in NICs should help pay for.

Whether directly or indirectly, the private sector will be able to contribute to the delivery of these large-scale projects and benefit as a result.

Beyond this, businesses will increasingly look to AI to solve their productivity issues, with early adopters likely to reap the most rewards.

And looking further ahead into 2026, a planned amendment to banking regulations could free up further access to loans for SMEs and infrastructure projects, with the potential to stimulate property prices.

Nottingham haulage company starts new journey following acquisition

A freight and courier company described by its acquirer as “a credit to the previous owners” has been sold.

Direct Sameday Services was founded in 1999 and utilises a fleet of modern vehicles to provide haulage and courier services across the UK and into Europe.

The company is headquartered in Bulwell on the outskirts of Nottingham, with a North West base in Rochdale, specialising in same-day parcel, pallet and tender document deliveries and employing over 60 staff.

Westland Assets is the acquirer of Direct Sameday, having been impressed by the business built up by co-founders Ian Gleave and Paul Tomkinson.

A lengthy search for a suitable acquisition opportunity by Westland Assets director David Whitefoot culminated in the deal for Direct Sameday.

“Of all the ones I have seen in the past two years, this is the best documented and most well-run business I have seen in a long time,” David told Motor Transport.

“The business was set up just over 25 years ago and considering the (industry) regulation that has followed since then, it is a credit to the previous owners.”

There are now ambitious plans to expand Direct Sameday, with David adding: “We have bought this business with the intention to scale up, not down.

“We want to grow the business in 2025 and 2026, make more investments in it and possibly expand it geographically. We have a vision of where we want to take this business.

“This strategic investment shows the commitment of investors, vision in the UK transport industry and understanding of all the future challenges ahead. We have full confidence in Direct Sameday Services, which has a bright future ahead in 2025.”

The transaction was advised on by KBS Corporate.

“I’m delighted with the result we managed to achieve for our clients,” said Joe Norris, KBS Associate Corporate Director. “It was far from easy at times, but I’d like to credit everyone involved in the deal on both the buy and sell side for their hard work and perseverance.

“We managed to overcome every issue and arrive at an outcome that worked for everyone.”

New year brings influx of tenants to Ednaston Park Business Centre

Ednaston Park Business Centre has welcomed an influx of new tenants.

With fellow occupiers comprising IT support and service specialists, Wytech Ltd, Bennet Samways Estate Agents, and creative agency, MacMartin, the Business Centre is now also home to L.T. VA Services LTD, EAL Engine Services, Dhesi Conveyancing Limited, D.A. Pak Limited and Gutu Mirror Limited, with more to be announced.

Virtual Assistant, Lisa Tenant from L.T. VA Services said: “After spending the last few years working from home with two teenage boys stealing the bandwidth and struggling to separate life from work, sometimes working 17 hours a day, I decided it was time for a change. Ednaston Park has given me that work-life balance I desperately needed, and the great Wi-Fi is an added bonus!”

Additionally, Light Science Technologies Holdings PLC (LSTH) have relocated from their office in Ednaston Park Business Centre to the brand new, Ednaston Barns. Completed at the start of 2024, the Barns sit within their own self-contained plot to the side of the Business Centre’s main building.

Simon Deacon, CEO at LSTH, said: “Light Science Technologies Holdings PLC was listed on the London Stock Exchange (AIM) 3 years ago and has seen significant growth.

“We have taken advantage of moving into the newly refurbished Byre at Ednaston Park Business Centre, which has been finished to a high standard, where we can continue our growth strategy in an idyllic working environment.”

In 2022, Clowes demolished the old nunnery living quarters at the back of the main building to create a further three units known as Ednaston Mews which are currently fully occupied.

Set in 18-acres of landscaped gardens, Ednaston Park Business Centre was built in the 19th century. Until 2016 it housed the St Mary’s Nursing Home; it was then bought by Clowes Developments in September 2017.

Since then, the developer has invested heavily in the property to turn it into modern office accommodation, combining contemporary styling with many of the building’s original period features.

Ednaston Park now comprises of flexible commercial space in the form of 29 office suites ranging in size from 54 sq ft to 553 sq ft, available as single or multi-office lets. It also features meeting rooms, a break-out area and landscaped gardens.

Workers in London earn by August what workers in the East Midlands earn in a year

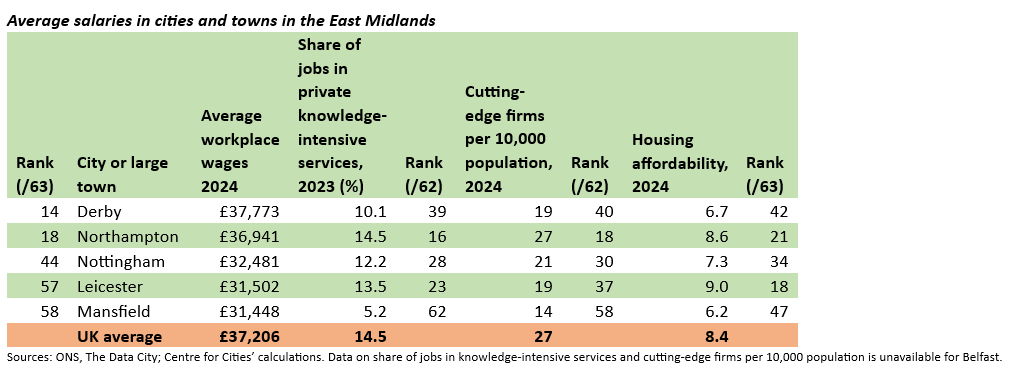

Cities Outlook 2025 today (20 January 2025) shows the stark pay divides in the UK. Average salaries of £49,500 in London are £16,800 above salaries in the East Midlands (£32,700), according to Centre for Cities.

This means that the average worker in London has earned by August what the average worker in the East Midlands will take a year to earn.

The pay divide primarily results from some cities having far more “cutting edge” private sector jobs and businesses than others. Places with the highest pay such as London and Cambridge have more than twice as many cutting-edge firms and up to three times as many cutting-edge jobs – in sectors like biotech and AI – as low pay places such as Leicester and Mansfield.

The scale of the pay divide underlines why 2025 has to be the year the Government delivers on its ambitions to raise economic growth. In Cities Outlook 2025, its latest annual outlook for urban economies in the UK, Centre for Cities urges the Government to follow through on its economic policy programme – including English devolution, the industrial strategy, and planning reforms.

Out of the 63 largest towns and cities, nearly all those with above-average salaries for the UK are in the Greater South East, including Reading and Milton Keynes. Just seven places in the rest of the country have salaries above the UK average – Leeds, Warrington, Derby, Swindon, Bristol, Aberdeen and Edinburgh.

Cities and towns where workplace wages are low have to address the barriers to growth in cutting-edge parts of their economy. This will require evidence-based assessments on the weaknesses in their local economies, prioritising work in high-skill over high-street activity and investing in fundamentals – such as skills, transport and workspace.

Cities Outlook 2025 also emphasises the importance of implementing the proposed changes to the national planning system to make housing delivery easier and quicker.

Lowering housing costs is a challenge for cities and large towns with high wages, including London and most places in the Greater South East: half of the ten places with the highest average wages also rank in the ten least affordable housing markets.

High housing costs eat into disposable incomes and raise barriers that prevent people moving to these areas to take advantage of the economic opportunities they offer.

Andrew Carter, Chief Executive of Centre for Cities, said: “The Government is right to identify boosting economic growth for every part of the country as a top priority. It is the only sustainable route to higher wages. But the stark nature of Cities Outlook’s findings shows an incremental approach is not going to be enough.

“Boldness, urgency and scale are crucial. 2025 needs to be year for delivery, particularly on the Government’s Industrial Strategy, framework for English devolution and its reforms to planning.

“Bold changes to planning rules can deliver more housing in the most expensive places and in our big cities, where it’s needed most. The Industrial Strategy must prioritise growing the cutting edge of the economy, and avoid calls to do something for all sectors and industries.

“And English devolution needs to be fast-tracked so more places, particularly the big cities, have the powers and resources to deliver the pay increases that many parts of the country badly need.

“This government has promised more money in people’s pockets. If people across the country are going to earn more by the end of the parliamentary term, then 2025 is year we need to see action and progress on the Government’s growth ambition.”

Out of the 63 largest towns and cities, nearly all those with above-average salaries for the UK are in the Greater South East, including Reading and Milton Keynes. Just seven places in the rest of the country have salaries above the UK average – Leeds, Warrington, Derby, Swindon, Bristol, Aberdeen and Edinburgh.

Cities and towns where workplace wages are low have to address the barriers to growth in cutting-edge parts of their economy. This will require evidence-based assessments on the weaknesses in their local economies, prioritising work in high-skill over high-street activity and investing in fundamentals – such as skills, transport and workspace.

Cities Outlook 2025 also emphasises the importance of implementing the proposed changes to the national planning system to make housing delivery easier and quicker.

Lowering housing costs is a challenge for cities and large towns with high wages, including London and most places in the Greater South East: half of the ten places with the highest average wages also rank in the ten least affordable housing markets.

High housing costs eat into disposable incomes and raise barriers that prevent people moving to these areas to take advantage of the economic opportunities they offer.

Andrew Carter, Chief Executive of Centre for Cities, said: “The Government is right to identify boosting economic growth for every part of the country as a top priority. It is the only sustainable route to higher wages. But the stark nature of Cities Outlook’s findings shows an incremental approach is not going to be enough.

“Boldness, urgency and scale are crucial. 2025 needs to be year for delivery, particularly on the Government’s Industrial Strategy, framework for English devolution and its reforms to planning.

“Bold changes to planning rules can deliver more housing in the most expensive places and in our big cities, where it’s needed most. The Industrial Strategy must prioritise growing the cutting edge of the economy, and avoid calls to do something for all sectors and industries.

“And English devolution needs to be fast-tracked so more places, particularly the big cities, have the powers and resources to deliver the pay increases that many parts of the country badly need.

“This government has promised more money in people’s pockets. If people across the country are going to earn more by the end of the parliamentary term, then 2025 is year we need to see action and progress on the Government’s growth ambition.”

Out of the 63 largest towns and cities, nearly all those with above-average salaries for the UK are in the Greater South East, including Reading and Milton Keynes. Just seven places in the rest of the country have salaries above the UK average – Leeds, Warrington, Derby, Swindon, Bristol, Aberdeen and Edinburgh.

Cities and towns where workplace wages are low have to address the barriers to growth in cutting-edge parts of their economy. This will require evidence-based assessments on the weaknesses in their local economies, prioritising work in high-skill over high-street activity and investing in fundamentals – such as skills, transport and workspace.

Cities Outlook 2025 also emphasises the importance of implementing the proposed changes to the national planning system to make housing delivery easier and quicker.

Lowering housing costs is a challenge for cities and large towns with high wages, including London and most places in the Greater South East: half of the ten places with the highest average wages also rank in the ten least affordable housing markets.

High housing costs eat into disposable incomes and raise barriers that prevent people moving to these areas to take advantage of the economic opportunities they offer.

Andrew Carter, Chief Executive of Centre for Cities, said: “The Government is right to identify boosting economic growth for every part of the country as a top priority. It is the only sustainable route to higher wages. But the stark nature of Cities Outlook’s findings shows an incremental approach is not going to be enough.

“Boldness, urgency and scale are crucial. 2025 needs to be year for delivery, particularly on the Government’s Industrial Strategy, framework for English devolution and its reforms to planning.

“Bold changes to planning rules can deliver more housing in the most expensive places and in our big cities, where it’s needed most. The Industrial Strategy must prioritise growing the cutting edge of the economy, and avoid calls to do something for all sectors and industries.

“And English devolution needs to be fast-tracked so more places, particularly the big cities, have the powers and resources to deliver the pay increases that many parts of the country badly need.

“This government has promised more money in people’s pockets. If people across the country are going to earn more by the end of the parliamentary term, then 2025 is year we need to see action and progress on the Government’s growth ambition.” Nottingham tram operator raises over £15,000 for local charities

Throughout 2024, Nottingham Express Transit (NET) raised more than £15,000 for a range of local charities and community initiatives in Nottingham, as part of its pledge to celebrate its 20th anniversary through an acts of kindness campaign.

As NET’s 2024 charity of the year, Nottingham Central Women’s Aid was a key focus for NET’s charity initiatives throughout the year. This included raising nearly £2,000 during a ‘walk the network’ initiative in May, which saw 30 members of the team walking along the tram network for over 13 miles from Hucknall to Clifton South.

NET also raised funds from its family fun day in August, and this Christmas, transformed a tram into a Santa’s grotto which welcomed 14 children and their mothers who are supported by the charity, for an afternoon of festive fun.

Alongside the charity of the year, NET team members were also encouraged to nominate their own chosen charities and take part in individual fundraising efforts.

Their efforts included supporting a fundraiser by 13-year old Lillie for the Brain Tumour Charity, a cause nominated by network controller Lee Wood. Meanwhile, experience agent John-Paul Redman raised £950 for When You Wish Upon a Star by walking 1,815 miles in 127 days.

The network also supported external fundraising efforts by Jacob Gadd, son of tram driver Alun Gadd, helping him to raise more than £2,000 for Our Dementia Choir. This charity has now been named as NET’s 2025 charity of the year.

Other group-wide donations included £700 towards Step Out Stay Out, giving more than £1,200 to Aspley food bank, and two separate donations of £1,000 to the Strelley Family Fun Day and Operation Polarised, an initiative in partnership with Nottinghamshire Police to support Nottingham’s youths ages seven to 17.

Rebecca Horne, business engagement manager at NET, said: “2024 has been a really strong year for us in terms of fundraising and we’re incredibly proud of the amount raised for so many worthy local causes.

“Central Women’s Aid, our charity of the year for 2024, was chosen by our colleagues and it’s been fantastic to see how much of a collaborative effort the team has put in to support them.

“Last year we also saw many of our colleagues undertake their own charitable work in support of a range of causes, and we will continue to champion this in years to come.”

Charge Cars acquired by consortium of private investors

Charge Cars, which was placed into administration on 31 May 2024, has been acquired by a consortium of private investors.

The creator of the ’67 – the all-new luxury, bespoke, electric muscle car – now plans to accelerate final development of the vehicle at its new global HQ in Silverstone.

Paul Abercrombie, CEO of Charge Cars, said: “On behalf of the consortium, I am delighted to announce the acquisition of Charge Cars.

“The ‘67 establishes a new class of EV – and we will now accelerate final development at our new global HQ in Silverstone, UK, rapidly delivering this exciting luxury vehicle to customers.

“The Charge brand has huge global potential, and we look forward to revealing more details very soon.”

The ’67 is designed and engineered from the ground up to create a new high performance luxury vehicle.

It is a hand-crafted car, with a body licensed by Ford Motor Company, combining American muscle car styling with an entirely new platform and the latest technology to captivate a new generation of sustainability-conscious automotive aficionados.

Toyota puts Derby’s Mayor and Deputy Mayor on the road in hydrogen-powered car

Toyota has lent Derby’s Mayor and Deputy Mayor a cutting-edge Mirai hydrogen fuel cell vehicle as their official car.

Toyota has been developing and trialling hydrogen fuel cell technology in a range of vehicles, including the prototype Hilux fuel cell pick-up truck designed and built at Toyota Motor Manufacturing UK in Burnaston.

Darius Mikolajczak, MD of Toyota Motor Manufacturing in the UK, said: “It is an honour for Toyota to support Derby City Council’s civic activities with the provision of a hydrogen fuel cell electric vehicle.

“We believe hydrogen plays a crucial role in decarbonising transport and is a key part of Toyota’s multipath approach to mobility. The Toyota Mirai, with its zero-carbon dioxide and no harmful tailpipe emissions, represents our commitment to sustainable technology and innovation. We are excited to see the positive impact this vehicle may have on inspiring the city’s journey towards a more sustainable future.”

Fuelled by hydrogen – extracted from water using zero carbon renewable energy produced at TMUK – the Mirai emits no carbon dioxide or harmful tailpipe emissions when in use. It is estimated that it will save a tonne of CO2 emissions over the trial, and with zero nitrogen dioxide and sulphur dioxide it will be supporting the city’s shift to zero and low emissions vehicles in their fleet.

Cllr Carmel Swan, Cabinet Member for Climate Change, Transport and Sustainability, praised the move. She said: “Our Climate Change Action Plan is all about how we can make changes to build a greener city and encourage partners and residents to do so as well. It’s only right that we lead by example, and I’m delighted that we’ve been able to work with Toyota to provide this brand new, zero emissions civic car at no cost to the Council.

“Our links with hydrogen go back centuries, with Henry Cavendish, who discovered the element, being buried in Derby Cathedral. Now, more than two and half centuries since that discovery, the use of this hydrogen powered car is another reminder of our place as a leader for sustainable fuel technologies.”

Hospitality business next to Nottingham’s Trent Bridge to be sold

Specialist business property adviser, Christie & Co, has been instructed to market Brewhouse & Kitchen bar and restaurant in Nottingham.

Situated in a prominent position on the A60 London Road into Nottingham city centre, adjacent to the River Trent and the iconic Trent Bridge cricket ground, Brewhouse & Kitchen is a large pub and restaurant housed within a characterful detached Victorian building.

The pub/restaurant is spread across four open-plan areas and seats 180 people inside, with an additional function facility on the first floor, seating a further 150 people, plus a large outdoor riverside terrace licensed for over 400 people.

There is scope to further develop the upper floors, including the two-bedroom owners’ apartment and the function space, into letting bedrooms (subject to planning consents).

The business currently operates as a wet-led establishment, which attracts trade from the surrounding districts and suburbs of Nottingham, as well as trade from visitors to Trent Bridge and Nottingham Forest FC City Ground on match days.

Neil Morgan, Senior Director – Pubs & Restaurants at Christie & Co, who is managing the sale, said: “This is a substantial character property, offering large internal trading areas as well as generous outside space, with seating for 200 on the riverside terrace and a customer car park.

“Due to its size and location, this opportunity will undoubtedly attract a broad range of buyers, from the traditional pub operators to casual dining/restaurant and ‘pubs with rooms’ buyers.”

The business is being sold as a virtual freehold with an asking price of offers in excess of £1,000,000.

Former Northampton Town FC chairman appears in court over fraud case

The former chairman of Northampton Town FC appeared in court yesterday (January 16) in connection with an investigation into an alleged £10.25m theft and fraud case.

David Cardoza was one of five men with former links to the redevelopment of the League One club due to appear at Northampton Magistrates’ Court on several counts of fraud and money laundering.

The other four included his father – 80-year-old former director Anthony Cardoza, who was excused from appearing at court in person.

Also in the dock was Howard Grossman, a 63-year-old property developer, his son – 37-year-old Marcus Grossman, and 54-year-old Simon Patnick.

No pleas were entered at the hearing and all five men were bailed to appear at Northampton Crown Court on 27 February, 2025.

The charges against the five defendants are as follows:

- All five are charged with conspiracy to commit fraud by false representation between September 2013 and April 2015. These relate to false representations, allegedly made to Northampton Borough Council, that money loaned by the authority to the football club would be used solely for developing Sixfields Stadium and an adjoining hotel, which were “untrue or misleading.”

- The Cardozas are also both charged with fraud by abuse of position, contrary to section 1 of the Fraud Act, which relates to a sum of £8.75m being paid from the football club to 1st Land Limited, a company owned by Howard Grossman.

- David Cardoza is further charged with transferring criminal property, namely £166,000 in a credit balance via a bank transfer from the bank account of Northampton Town Football Club Limited, knowing or suspecting it to constitute or to represent, in whole or in part, directly or indirectly, the benefit from criminal conduct.

- In addition to fraud, Howard Grossman faces three charges of transferring criminal property, specifically amounts of £650,000 from the bank account of his company County Homes (Herts) Ltd to his son and fellow director, Hayden Grossman, as well as transferring £10,000 from 1st Land Limited to Simon Patnick and £15,000 from 1st Land Limited to Simpa Investments Limited, a company owned by Simon Patnick.

- Mr Grossman and his son Marcus are further charged with transferring criminal property, namely £20,000, from Marcus Grossman’s account to Simon Patnick, knowing or suspecting it to constitute or to represent, in whole or in part, directly or indirectly, the benefit from criminal conduct.

- As well as fraud, Patnick is accused of acquiring criminal property contrary to the Proceeds of Crime Act 2002, namely £61,800 in credit balances via bank transfers from or on behalf of Howard Grossman and Marcus Grossman knowing or suspecting it to constitute or to represent, in whole or in part, directly or indirectly, the benefit from criminal conduct.

- Howard Grossman faces the same allegation, relating to a sum of £10,000 transferred to Margro Properties Ltd, a company run by Marcus Grossman.

2025 Business Predictions: Iain Hibbert, CEO, Devello Group

It’s that time of year, when Business Link Magazine invites the region’s business leaders to offer up their predictions for the year ahead.

It has become something of a tradition, given that we’ve been doing this now for over 30 years.

Here we speak to Iain Hibbert, CEO at Devello Group.

In 2025 the UK property market is projected to experience moderate growth, influenced by factors such as easing borrowing costs, stamp duty changes and regional variations. However, these factors are susceptible to change as the impact of the Autumn budget works its way through. Key predictions include:

Mortgage Rates: Average two- and five-year fixed mortgage rates are projected to decrease to around 4% by the end of 2025, enhancing buyer affordability and confidence.

House Price Growth: House prices are expected to rise by 2% to 4% in 2025, driven by reducing mortgage interest rates.

Stamp Duty Land Tax Changes: From 1 April 2025 SDLT thresholds will be lowered, increasing moving costs for many buyers. This may lead to a surge in transactions before the deadline followed by a potential slowdown.

Investor Considerations: Increased SDLT surcharges for second homes and potential regulatory changes may influence investment decisions, particularly in the buy-to-let sector.

Rental Market: Rents are forecasted to rise by approximately 17.6% between 2025 and 2029, outpacing wage growth, due to persistent supply-demand imbalances.

Planning and Development: Due to the significant “shake up” introduced in the form of the new National Planning Policy Framework 2024, and the Government’s pledged commitment to delivering 1.5 million new homes, activity in this sector is expected to be both significant and buoyant with land promotion taking centre stage. This may be hampered however by the ability of the planning system to cater for the increased volume of applications and appeals.

Overall, we think the 2025 UK property market is set for steady growth, with regional disparities and policy changes playing significant roles in shaping market dynamics, despite what is expected to be a year of general economic stagnation.